Two Countries, One Basin, Two Futures

Why Suriname can’t take off

eyesonguyana

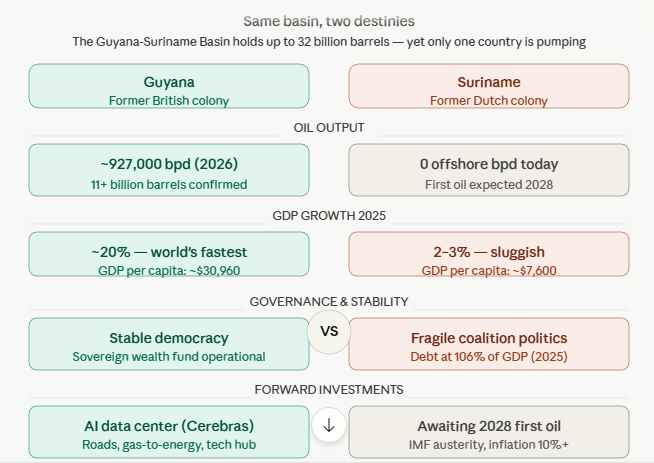

They share a border, a coastline, a geology, and a dream. Both Guyana and Suriname sit perched on the northern rim of South America, two small, sparsely populated nations that for most of their post-colonial histories ranked among the poorest on the continent. Then the offshore drilling rigs arrived, and everything changed — but only for one of them.

Today, Guyana is the world’s fastest-growing economy, pumping nearly a million barrels of oil per day and signing deals for AI data centers. Suriname is still waiting for its first drop of offshore crude, crushed under debt, shaken by street riots, and haunted by the ghost of a dictator-turned-president who looted the national treasury. The contrast is so stark that economists have begun using the two neighbors as a real-time natural experiment in the question that haunts every resource-rich developing nation: does oil save you, or destroy you?

The Geological Lottery — And Why a Ticket Isn’t Enough

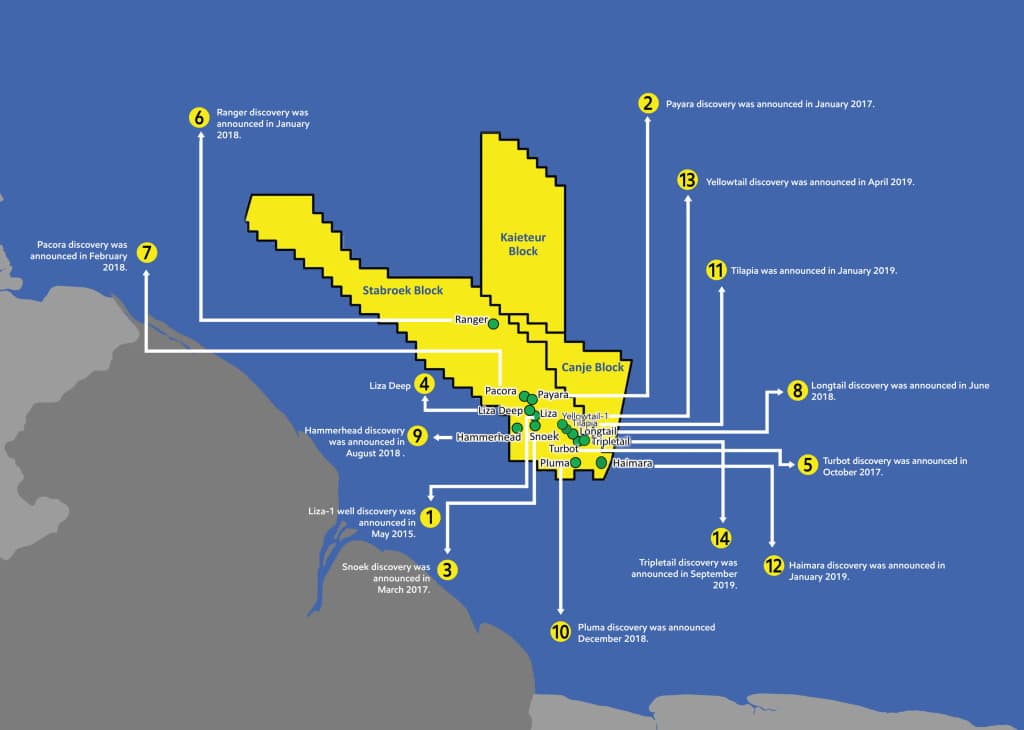

To understand why Guyana succeeded and Suriname has not, start underground. Both countries share what geologists call the Guyana-Suriname Basin, an ancient underwater geological formation that turned out to contain one of the most spectacular concentrations of light, sweet crude oil on earth. The U.S. Geological Survey initially estimated the basin held around 15 billion barrels. They were wildly wrong — in the optimistic direction.

After a swathe of high-quality discoveries in the offshore Stabroek Block, Guyana’s government finds itself managing one of the world’s largest oil booms. In roughly a decade, the country went from its first oil discovery to South America’s third-largest oil producer. By late February 2026, Guyana was lifting 926,550 barrels per day, with four more projects under development expected to push output to 1.7 million barrels per day by 2030.

Related Posts:

Suriname, meanwhile, sits just to the east of this bonanza and possesses what its own state oil company, Staatsolie, estimates could be as much as 30 billion barrels of recoverable oil resources — with TotalEnergies’ Block 58 development potentially producing 200,000 to 500,000 barrels per day. On paper, Suriname’s geological endowment is arguably even larger than Guyana’s.

But geology and destiny are not the same thing.

The quality of oil matters enormously. Guyana’s crude oil from the Liza field has been confirmed as “high quality,” meaning it is sweet — with low sulfur content — and light — with a high API gravity. Sweet light crude is the preferred type from which the highest-value petroleum products are derived. The Stabroek Block’s oil has an API gravity of 31.9 degrees and 0.59% sulfur content — crucial characteristics in a world where strict emission standards make it costly and complex to refine heavier, sourer crude oils into low-emission fuels.

Suriname’s oil is also attractive — discoveries in Block 58 are comprised of medium to light sweet crude oil and condensates with API gravities of 34 to 60 degrees and low sulfur content, characteristics similar to the crude found by ExxonMobil in the neighboring Stabroek Block. The raw material, in other words, is comparable. The problem is everything that comes before and after it leaves the ground.

The Drilling Problems Nobody Predicted

Here is where Suriname’s misfortune begins. When TotalEnergies and APA Corporation began drilling in Block 58 after a January 2020 discovery announcement, expectations were sky-high. Suriname’s president was predicting first oil by 2025. Then the drills told a different story.

TotalEnergies and APA chose to delay the final investment decision for developing the Sapakara and Krabdagu oil discoveries due to poor drilling success, the high gas-to-oil ratio of some discoveries, and a mismatch between seismic data and drilling results. The seismic maps had suggested one geology; the actual rock layers produced another. Too much of what they found was natural gas rather than the easier-to-monetize crude oil. This delayed not just Suriname’s oil boom but its entire economic recovery plan.

It took until October 2024 — two full years later than expected — for TotalEnergies to finally approve the $10.5 billion Final Investment Decision for the GranMorgu project. Block 58 oil is now expected to start in 2028, leading to a doubling of real GDP by 2030.

Meanwhile Guyana experienced the opposite of Suriname’s drilling disappointments. It took a mere four years for Guyana to go from its first discovery in 2015 to first oil in 2019 — incredible because it usually takes a decade or longer for development of billion-dollar offshore energy projects. ExxonMobil kept finding more oil with almost every drill. Estimates today suggest the Stabroek Block has about 11 billion oil-equivalent barrels of reserves, and Exxon expects daily production to top one million barrels before the end of 2026.

The lesson here is sobering: even in the same basin, geology is not uniform. The same rocks that yielded a clean bonanza for Guyana threw curveballs at Suriname’s drillers. And crucially, when your country is already in economic crisis, a two-year delay in the FID is not a technical inconvenience — it is a political catastrophe.

The Ghost in the Machine: Decades of Institutional Rot

Suriname’s geological bad luck would be manageable if the country had strong institutions to weather the wait. It does not, and understanding why requires a painful excursion into the country’s recent history.

Suriname’s economic downturn commenced during President Dési Bouterse’s final years, a period marked by considerable policy mismanagement, public sector debt buildup, a shrinking currency, and high-level corruption. The incoming Santokhi government inherited a debt default, a depleted national treasury, and rising inflation.

Bouterse is one of the most extraordinary figures in modern Latin American politics — a military coup leader, convicted murderer, convicted drug trafficker (in absentia in the Netherlands), and twice democratically elected president. The U.S. government’s International Narcotics Control Strategy Report stated: “Corruption pervades many government offices in Suriname.” This comes from the top, as Bouterse’s checkered track record reflects a lack of playing by the rules, beginning with his involvement in the 1980 coup, the December 1982 massacre of 15 leading members of the opposition, and a conviction in the Netherlands in 2000 for cocaine trafficking.

Since December 2015, Bouterse took out at least 17 loans from the IMF, Eximbank China, and other lenders. He borrowed with the recklessness of a man who did not expect to be held accountable — and for a long time, he was not. This debt reached crisis proportions in the 2010s. Private lenders and international financial institutions queued up to make loans, often at high interest, amid the deep crash of global commodity prices.

When he was finally voted out in 2020, the wreckage was immense. Bouterse’s successor Santokhi inherited a major mess in both economic and governance terms, followed by several tough years of economic austerity, structural adjustment, and lengthy debt renegotiations. Suriname effectively entered the oil era already bankrupt.

Having made important earlier progress to restore macroeconomic stability, fiscal and monetary slippages in 2025 reduced cash buffers, weakened the currency, and increased inflation back to double digits. The increase in gross debt to an estimated 106% of GDP is mainly due to a successful liability management operation. In plain English: even Suriname’s debt restructuring deals have added to the debt pile.

The contrast with Guyana is almost cruel. Guyana’s success was built over two decades of trust and consistent policy. By partnering early with an ExxonMobil-led consortium and maintaining a stable, predictable contractual environment, Guyana allowed capital and expertise to flow rapidly. The economic results speak for themselves: GDP growth of nearly 20% in 2025 and a projected 16.2% in 2026, making Guyana the fastest-growing economy in the world.

How You Deploy Oil Revenue: The True Divide

The most revealing difference between the two countries is not what they have found underground, but what they have done with the revenues already flowing — or in Suriname’s case, not flowing.

Guyana moved fast, built institutions, and invested. Guyana’s Natural Resource Fund was established to manage oil revenues for long-term development. As of 2025, the fund exceeds $2 billion with strict withdrawal rules to ensure intergenerational equity. The government has channeled oil money into roads, hospitals, an energy grid, and now — most ambitiously — artificial intelligence infrastructure.

The Government of Guyana and Cerebras Systems signed a landmark Memorandum of Understanding to build and operate a state-of-the-art artificial intelligence data center of up to 100MW in Wales, Guyana — a transformative initiative marking a new chapter in Guyana’s journey to become an AI-first nation and the regional leader in digital innovation. In 2025, the government’s income from oil — profits and royalties — was estimated at about $2.5 billion, a staggering sum for a country of around 800,000 people, now accounting for more than a third of the national budget.

Suriname, by contrast, is still arguing about how to operationalize a Savings and Stabilization Fund that does not yet have oil to save. The IMF has been blunt about what needs to happen first. The IMF has called for Suriname to implement its Public Financial Management Priority Action Plan, operationalize its Savings and Stabilization Fund, and remove electricity subsidies to provide resources for social assistance and growth-enhancing investments.

The resource curse looms as a real threat: when poor countries become reliant on new fossil fuel revenue, it leaves them vulnerable to global price fluctuations, and governments sometimes embezzle or misuse oil money rather than sharing it with citizens. Suriname has already lived through one version of this curse with its gold and bauxite revenues. The question is whether it can break the cycle before the oil arrives.

The Clock That Is Running Out

There is an uncomfortable dimension to Suriname’s delay that goes beyond economics: the global energy transition is underway, and the window for new oil producers to capitalize on fossil fuel demand may be narrowing.

A combination of uncertain drilling results, high development costs, and pressures to curb carbon emissions, coupled with the threat of peak oil demand, is weighing heavily on investment in offshore frontier oil basins. Offshore Suriname may be the hottest frontier in South America, but there are signs that time is running out for the country to explore that vast offshore petroleum potential.

Guyana, by moving fast, has locked in a decade of oil revenues that will transform its economy regardless of what happens to global oil demand in the 2030s and 2040s. Suriname, arriving at the party nearly a decade later, will have fewer years to benefit from high prices — and will need to spend much of its early revenue simply paying off debts rather than building the future.

Can Suriname Still Catch Up?

The picture is not entirely bleak. Recent legal reforms and plans for a Savings and Stabilization Fund are intended to ensure transparent management of future oil revenues. The fiscal potential is significant — oil could provide the means to restore macroeconomic stability, invest in infrastructure, and reduce debt pressures.

The oil discovered in Block 58 is particularly attractive to exploit because it is light, with an API gravity of around 34 degrees, and sweet with low sulfur content, making it cheaper and easier to process into high-quality, low-emission fuels — exactly the kind of crude that will retain market value longest into an era of tightening environmental standards.

And there is reason to think Suriname’s geology may have more secrets. Block 58 lies contiguous to the prolific Stabroek Block in offshore Guyana, where Exxon discovered at least 11 billion barrels of oil. There is considerable speculation that the abundant petroleum fairway contained in that oil block continues into Block 58. If it does, Suriname could find itself sitting atop reserves comparable to Guyana’s — and with the infrastructure and experience that Guyana’s early development has generated nearby.

But geology only matters if governance works. The country’s IMF overseers have spelled out exactly what is required: anti-corruption reforms, an independent environmental regulator, a functioning sovereign wealth fund, civil service reform, and transparent public investment management. These are not exotic demands — they are the basic infrastructure of a functional petro-state.

The Lesson Written in Crude

The story of Guyana and Suriname is, ultimately, a story about what countries are made of before the oil arrives. Guyana had two decades of stable democratic governance, consistent contractual relationships with foreign investors, and — crucially — the institutional good sense to let ExxonMobil move fast. The reward was a four-year discovery-to-first-oil sprint that stunned the industry.

Suriname had two decades of Bouterse: coups, corruption, drug trafficking, borrowed money spent on patronage, and a treasury stripped bare just as the offshore drills began to turn. The reward was a country forced into IMF austerity at the precise moment it needed to be investing in its oil future — and a first-oil date that keeps slipping further into the future.

Oil does not save countries. Institutions do. Guyana had them. Suriname is still building them — and the clock is ticking.